Quarterly Commentary 4Q’25

The Alphabet Economy

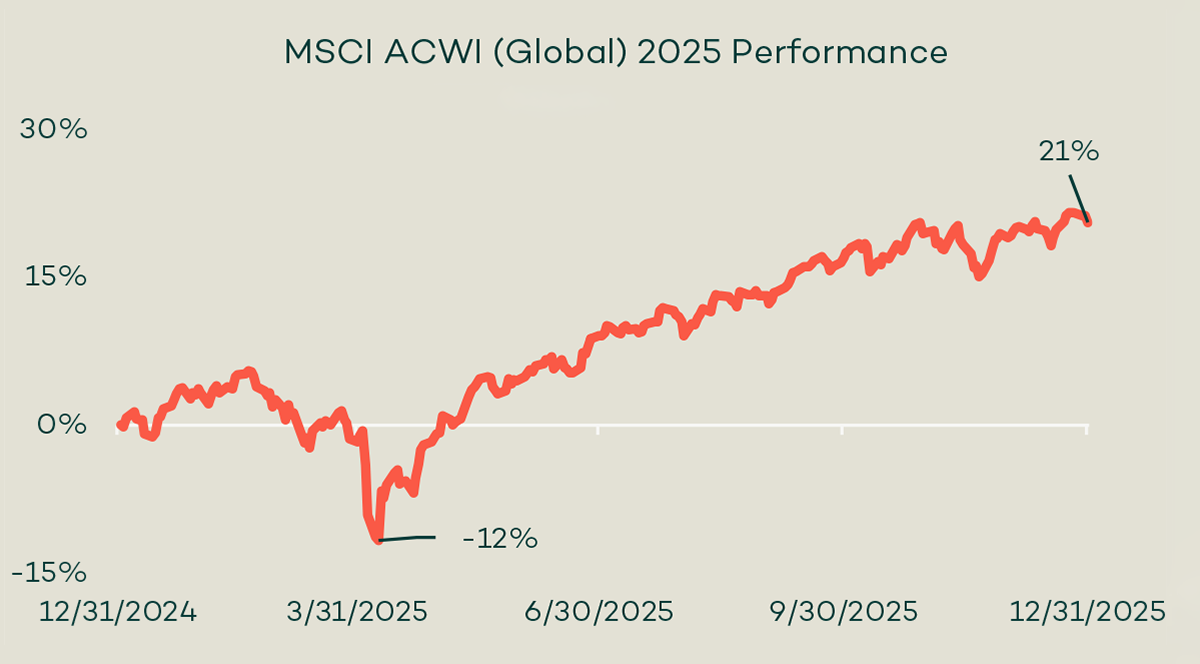

Wall Street has a fetish for shorthand. In 2025, it involved letters. Take “V-shape,” code for large-cap equities’ torrid bounce after April’s tariff scare (see chart). By year-end, the V was complete: the MSCI ACWI finished up roughly 21%, and U.S. equities gained about 16%. On the one hand, that outcome is surprising given the elevated level of policy uncertainty and persistently negative news. On the other hand, the performance drivers weren’t new. Continued earnings growth, AI investment, and fiscal support carried over from late 2024, allowing markets to look past the noise and refocus on fundamentals.

For bonds, the letter was “H” for higher-for-longer interest rates. While rate cuts supported short- and intermediate-duration bonds—lifting the Bloomberg U.S. Aggregate Bond Index by roughly 7%—longer-dated Treasuries told a different story. Bonds with 20+ year maturities fell about 1%, as persistent budget deficits, increased issuance, and an unpredictable policy backdrop pushed investors to demand higher yields for long-term lending.

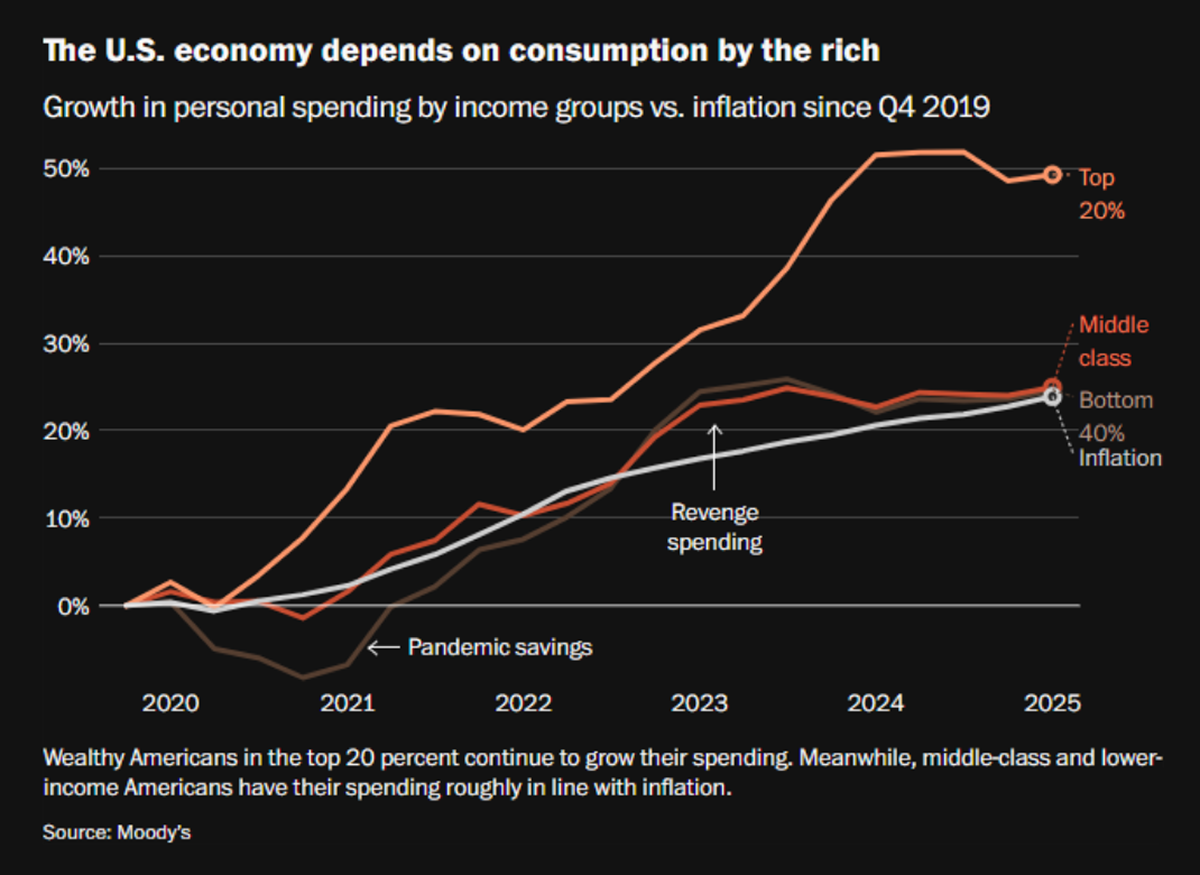

On the economy, the chosen letter was "K”—a year where growth was real, but uneven. Households at the top of the income and asset spectrum continue to benefit from strong wage gains and rising financial wealth, while lower-income cohorts face slower wage growth and rising credit stress. This partially explains the disconnect between headline macro data (which points to resiliency) and the lived experience of many consumers, who increasingly feel left behind*.

A Moody's** report reinforced this divergence. The highest-earning 20% of households now account for ~50% of total consumer spending (see chart left), with strength concentrated in discretionary categories such as travel and leisure. By contrast, spending growth among middle- and lower-income consumers has been slower. Credit conditions tell a similar story: prime, higher-FICO borrowers remain resilient, while stress continues to build in subprime cohorts. Wage growth follows the same pattern, with higher-income earners outpacing inflation while lower-income wages lag behind.

Our view for 2026 is that the economic picture does not yet appear threatening. Corporate earnings growth has reasserted itself, consumer spending continues (albeit unevenly) and financial stress remains contained. Inflation has moderated but not fully dissipated. That said, risks are building beneath the surface. A sharper-than-expected labor slowdown and/or a loss of confidence in the AI investment cycle would matter precisely because so much of today’s growth rests on the narrow upper end of the K.

At the same time, inflation and affordability pressures remain concentrated at the lower end of the income spectrum. If price pressures prove sticky enough to limit the pace of rate cuts, lower-income households face a double bind: weaker real wage growth alongside borrowing costs that stay higher for longer. That combination raises the risk that localized stress spills into broader economic activity—ultimately weighing on confidence, asset prices, and the wealth effects supporting spending at the top. For us, this reinforces the case for portfolios built around high-quality businesses with durable moats, strong balance sheets, and products or services that remain relevant across economic regimes.

Constructing a Resilient Portfolio

Our managed global stock portfolios kept pace with major indices during the quarter, reflecting a strategy we've emphasized for several years: increasing global and industry diversification while staying focused on enterprising, sustainable businesses. Healthcare was a standout in 4Q as investors grew more comfortable with a familiar set of headwinds—including Medicaid cuts, pricing policy uncertainty, and elevated funding costs. Against that backdrop, GSK PLC, Waters, and AstraZeneca outperformed. Alternative-energy holdings First Solar and Nextpower also contributed, supported by sustained electricity demand as the AI infrastructure build-out continues despite policy concerns.

Headwinds were concentrated in consumer-exposed areas. DR Horton and Aptiv lagged as a decelerating labor market weighed on near-term growth expectations. Defensive holdings such as Costco also trailed amid ongoing debate about relative growth versus valuation.

In the 4th quarter, we started three new positions:

S&P Global (SPGI): a dominant provider of financial and sustainability data with a durable competitive moat and highly recurring revenue through its Ratings business. We view SPGI as a critical enabler of sustainable finance, supplying the data, benchmarks, and climate analytics required for transparent global disclosure.

Boston Scientific (BSX): a leader in minimally invasive medical technologies delivering consistent organic growth. We see BSX as a contributor to improved health outcomes and greater health equity, with innovation that lowers long-term system costs and reduces the environmental footprint of care.

Workday (WDAY): a scalable human capital management platform embedded in core enterprise systems. As a system of record for workforce and pay data, Workday enables more consistent governance, disclosure, and insight into human-capital practices..

These companies give us exposure to secular growth themes—healthcare innovation, corporate data infrastructure, and workforce management—with business models less sensitive to near-term economic swings. We funded these additions by trimming several outsized positions—including Alphabet, Trane Technologies, Corning, and Flex—names that have benefited directly or indirectly from elevated AI-related investment.

COP'n an attitude

The mood at this year’s Conference of the Parties (COP30) in Belém, Brazil, was dour.iii Billed as a “COP of truth and implementation,” the summit instead exposed deep fractures. Major emitters failed to agree on explicit language to phase out fossil fuels, and efforts by the European Union and roughly 80 countries to signal a clearer transition away from coal, oil, and gas ultimately went nowhere. While the final agreement preserved climate diplomacy and included incremental progress, particularly around adaptation finance, it stopped well short of delivering a credible roadmap for the global energy transition. The absence of the United States and China’s decision to remain largely on the sidelines only reinforced the sense of drift.

The mood at this year’s Conference of the Parties (COP30) in Belém, Brazil, was dour.*** Billed as a “COP of truth and implementation,” the summit instead exposed deep fractures. Major emitters failed to agree on explicit language to phase out fossil fuels, and efforts by the European Union and roughly 80 countries to signal a clearer transition away from coal, oil, and gas ultimately went nowhere. While the final agreement preserved climate diplomacy and included incremental progress, particularly around adaptation finance, it stopped well short of delivering a credible roadmap for the global energy transition. The absence of the United States and China’s decision to remain largely on the sidelines only reinforced the sense of drift.

Having followed these meetings for years, we know progress is rarely linear. Climate negotiations move in fits and starts, and this year felt more like a step back than forward. But policy summits are only one input. The real test of the transition shows up in deployment, cost curves, and capital allocation.

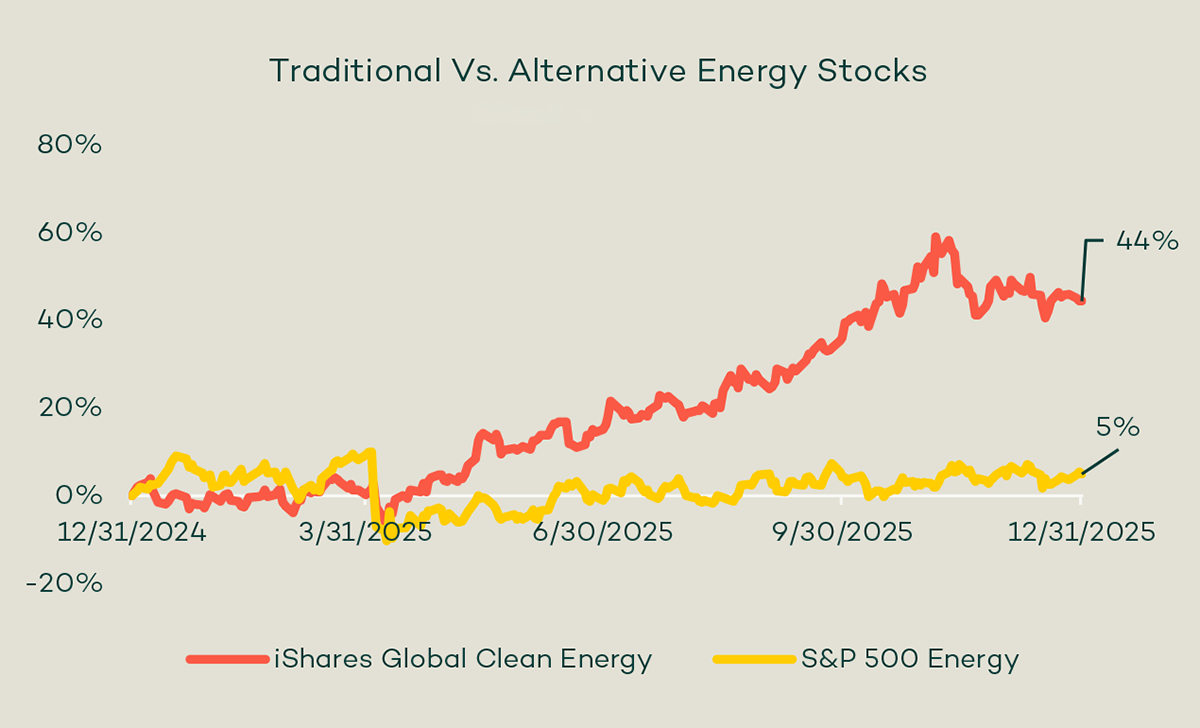

On that front, the signal was clearer. The global buildout of clean energy continued at a rapid pace in 2025, with solar and wind accounting for the vast majority of new electricity generation.**** Falling technology costs, energy security concerns, grid investment, and the power demands tied to digital infrastructure are pushing capital toward renewables regardless of the pace of global consensus. Markets reflected this reality: clean energy equities materially outperformed traditional energy over the year (see chart).

Fossil fuels remain central to the global energy system, and the transition will not be smooth or uniform. But COP30 underscored the limits of politics. The market’s message was more decisive: the energy transition is increasingly being driven by economics as much as by policy.

* University of Michigan's Index of Consumer Sentiment and The Conference Board's Consumer Confidence Index** Moody’s Analytics review of Federal Reserve Data, Bloomberg, WSJ*** https://www.nytimes.com/2025/11/22/climate/cop30-climate-summit-ends-belem.html**** https://ember-energy.org/latest-insights/highlights-of-the-global-energy-transition-in-2025You should always consult a financial, tax, or legal professional familiar with your unique circumstances before making any financial decisions. This material is intended for educational purposes only. Nothing in this material constitutes a solicitation for the sale or purchase of any securities. Any mentioned rates of return are historical or hypothetical in nature and are not a guarantee of future returns. Past performance does not guarantee future performance. Future returns may be lower or higher. Investments involve risk. Investment values will fluctuate with market conditions, and security positions, when sold, may be worth less or more than their original cost.