Quarterly Commentary 1Q’26

Long Day's Journey into… Volatility

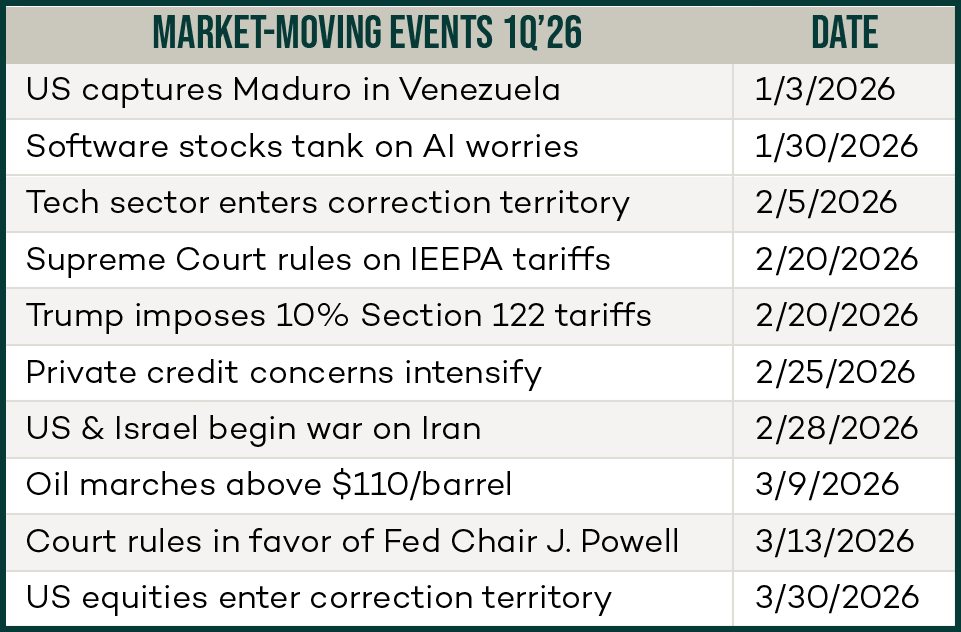

The first quarter of 2026 began with a covert military operation on one continent and ended with an overt one on another. As the chart to the right illustrates, nearly every trading week brought a new shock. Some were norm-breaking, like the White House's pressure campaign on the Fed; some potentially systemic, like the fractures emerging in private credit. Each one forced markets to reprice risk before the last shock had fully settled. By any measure (volatility, drawdown, dispersion, number of events), it was the most eventful – and nerve-rattling – quarter in recent memory.

Since last fall, and based on key market indicators, we’ve been tracking a rotation away from large-cap US growth stocks and toward international and smaller-cap equities. We’ve also been calling a rise in stock price volatility (see here and here). These were the stories we expected to define 2026, and early price action confirmed them.

Then came February 28th and the bombing of Iran, diverting the world’s attention and the market’s trajectory. What began as economic friction (tariff rulings, private credit stress, AI exhaustion) escalated into something harder to price: the geopolitics of ongoing military action and outright war. By late March, oil prices had become the stock market’s primary driving variable. The US and Israeli attacks on Iranian infrastructure effectively closed the Strait of Hormuz, through which 20% of global crude supply flows. Energy prices surged as did the price of fertilizers and other key feedstocks, sparking fears of runaway global inflation and potential food shortages.

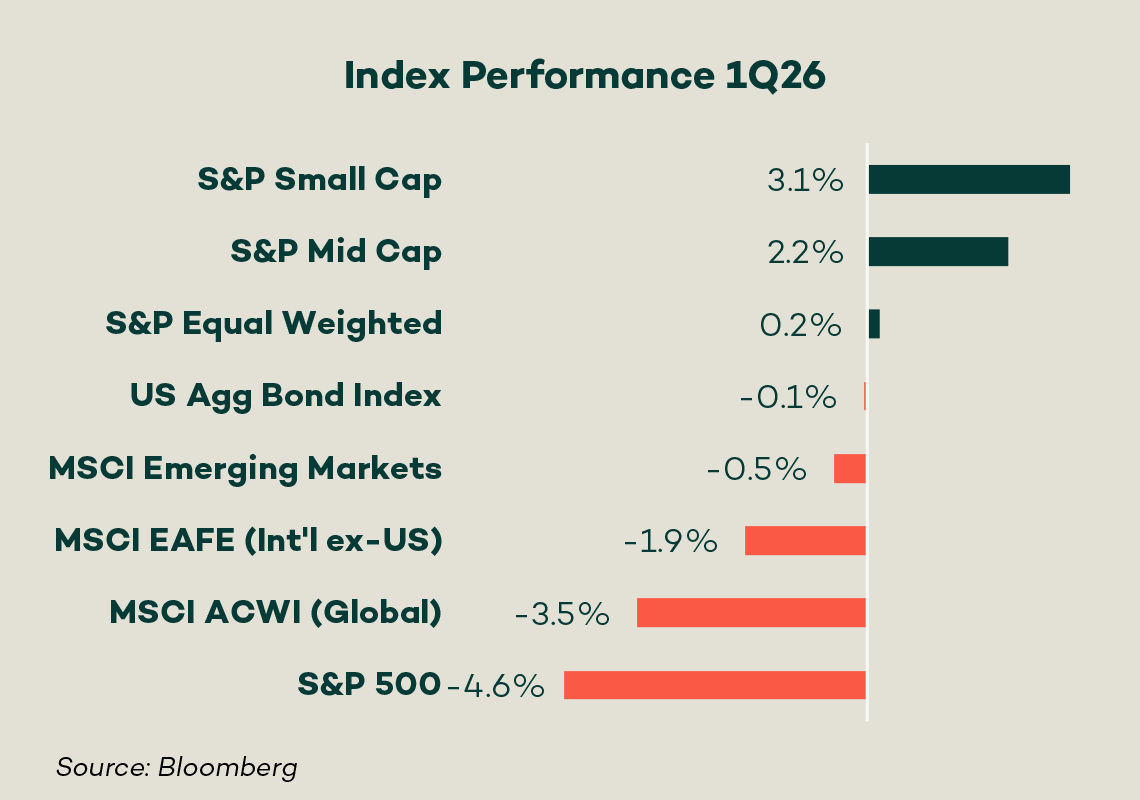

With "mission accomplished" turning to "mission impossible" as March proceeded, markets moved dramatically, with bond yields and stock prices swinging wildly on every major news update. By the end of the quarter on March 31, US and global large-cap indices were both down, -4.6% and -3.5%, respectively. US small and mid-cap stocks did better, returning 3.1% and 2.2% respectively, largely because of outsized exposure to energy. Bond investors (Barclays Agg) gave back much of their quarterly gains as yields rose amid fears of a prolonged Middle East conflict that could reignite energy-driven inflation.

As we write, the war in Iran is ongoing, raising new risks: rising inflation and interest rates, a potential hit to global GDP, and erosion of confidence in US leadership. The closing of the Strait of Hormuz has disrupted oil and gas supply in ways that affect Europe and Asia far more than the U.S. — and as a result, the rotation favoring international stocks has, perhaps temporarily, reversed. We cannot know when or how these dynamics will resolve. Importantly, our approach doesn't rely on prediction — it relies on preparation.

In that spirit, we are staying geographically diversified. Because risks are shifting everywhere, balance is the best way to navigate uncertainty — and we know that from deep experience. We don't take lightly that behind these market dynamics are real human lives and real suffering. Our role is to hold both the weight of what's happening in the world and the responsibility to guide our clients through it with steadiness and care.

Portfolio Positioning & Preparation

In this time when not owning defense and oil stocks is a headwind for social investors, Figure 8’s Global Equity strategy kept pace with major benchmarks. Our stock portfolios benefited from a balanced approach across geographies, styles, and themes. Positive contributors included tech infrastructure names such as Corning, Taiwan Semiconductor, and ASML Holdings. Our alternative energy-focused and aligned companies, HA Sustainable Infrastructure, Amalgamated Bank, and Nextpower Inc, performed exceptionally well following strong earnings reports and acted as a natural hedge against surging oil prices. Materials stocks also exhibited strength, with Linde demonstrating operational excellence and a robust high-quality project backlog.

On the flip side, a handful of portfolio companies were caught in the agentic AI narrative that took hold in February. Investors are wary of the possibility that AI agents may ultimately replace major functions now provided by software companies like Adobe and Workday, financial data companies like Intercontinental Exchange and S&P Global, and payment networks like Visa and Adyen. As a result, the shares in those names traded lower. Our analysis is that the sell-off in these names is overdone. AI will impact business models, no doubt, but the downturn does not account for how deeply embedded these businesses are in the economy – or the ability of the companies to innovate to meet customer demand.

Our portfolio team was active throughout the quarter, adding to higher-conviction names and trimming holdings we deemed fairly valued or least aligned with our rotation thesis. In addition to a broad rebalancing, we initiated three new positions:

ServiceNow: we are attracted by its high-margin recurring revenue model and a $275B market we believe will expand meaningfully through enterprise agentic AI adoption, driving sustainable productivity gains across complex workflows

Vertex Pharmaceuticals: we believe this is one of the clearest growth stories in healthcare, with sector-leading revenue visibility anchored by cystic fibrosis dominance and a breakthrough non-opioid pain pipeline addressing significant unmet medical needs

Danone: we are drawn to its leadership in specialized nutrition and high-growth probiotics, diversified and resilient cash flows, and strong alignment with our long-term sustainability mandates

Life and Energy During Wartime

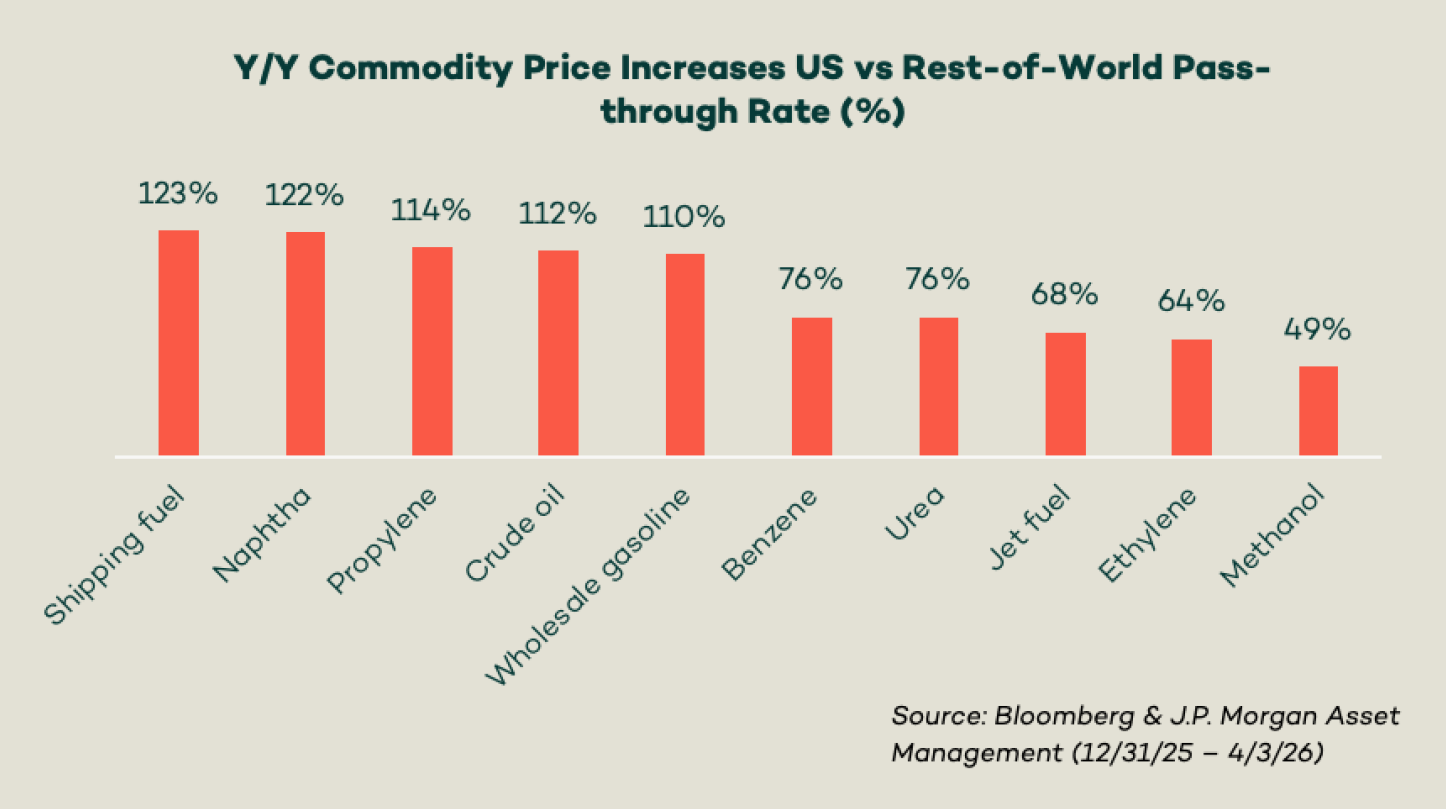

War in Iran has created a new urgency for energy demand around the world, including the U.S. The war has exposed a deep-seated fragility in the US energy market, one that runs counter to what we hear from the government and news media. A recent J.P. Morgan “Eye on the Market” report for April 2026 put it plainly: US fossil fuel independence is not the economic firewall we were promised. Despite being a net exporter of fossil fuels, the US is not immune to global price volatility. Year-to-date, US price increases for wholesale gasoline, shipping fuel, naphtha, and petrochemicals have matched or in many cases exceeded those in Europe and Asia (see chart next page). In other words, when the Strait of Hormuz is held hostage, global hydrocarbon chains reprice instantly and the impacts are felt universally.

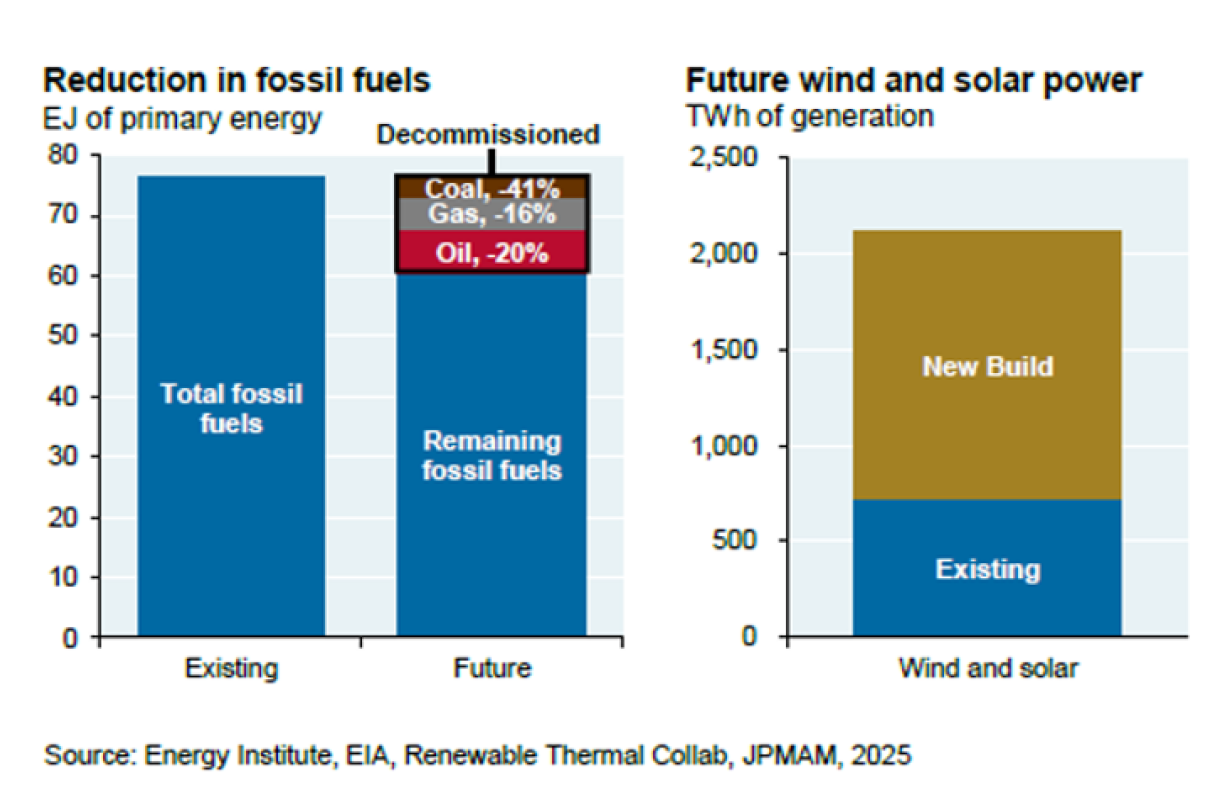

The war-related energy price surge, even if temporary, highlights the economic vulnerability related to fossil fuels. It also strengthens the case for renewable energy not just as a climate or cost argument, but as a matter of energy security. The same J.P. Morgan report illustrates both the opportunity and the scale of the challenge: a plausible decarbonization path would cut total US fossil fuel consumption by roughly 20%, with coal consumption falling 41%, gas 16%, and oil 20% (see chart below). Getting there would require cuts in coal- and gas-power generation, replacing internal combustion engine vehicles with EVs, and converting a meaningful share of residential and commercial heating to electric heat pumps powered by renewables. It would also require wind and solar capacity to triple from current levels (a build-out of roughly 14 years at today's pace). The war doesn't change this math, but it compresses the timeline: higher prices and security concerns add new urgency to a transition that was already going to take a decade-plus of massive-scale investment. If the US wants true energy independence (and the security that goes with it), building out renewable infrastructure is part of that answer, not separate from it.

We see three areas where the thesis translates most directly into portfolio exposure. Grid modernization is the most obvious because every new gigawatt of renewables, every new data center load, and every EV fleet puts pressure on infrastructure that in many regions has not been upgraded in decades. Energy storage, particularly via battery energy storage systems, is now a core renewable energy system requirement; without it, intermittent generation cannot substitute for dispatchable fossil capacity at scale. And distributed generation – which includes rooftop solar, behind-the-meter storage, microgrids, and combined heat and power – offers offer localized resilience that looks increasingly attractive when the global grid feels fragile.

This is further support for our clean energy thesis, and we will continue to invest across these themes as we work toward a safer, more resilient world. As the war in Iran proceeds, we expect continued price volatility in anything related to energy supply. A deceleration in the conflict would likely reduce oil prices and might even present near-term buying opportunities to build on our exposure to the long-term clean energy transition. For many reasons, we hope for that path toward peace.

You should always consult a financial, tax, or legal professional familiar with your unique circumstances before making any financial decisions. This material is intended for educational purposes only. Nothing in this material constitutes a solicitation for the sale or purchase of any securities. Any mentioned rates of return are historical or hypothetical in nature and are not a guarantee of future returns. Past performance does not guarantee future performance. Future returns may be lower or higher. Investments involve risk. Investment values will fluctuate with market conditions, and security positions, when sold, may be worth less or more than their original cost.